Revenue to the public treasury is the sum of the following sources:

| Revenue Area | 2014-2015 Amount (January 2015 Estimates) |

|---|---|

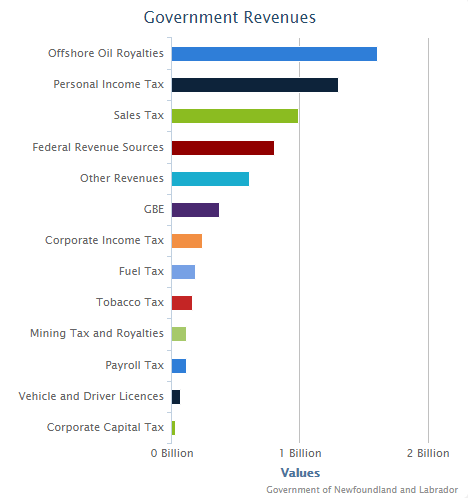

| Offshore Oil Royalties | $1,518,279,972 |

| Personal Income Tax | $1,307,650,000 |

| Sales Tax | $989,097,000 |

| Federal Revenue Sources | $806,825,000 |

| Other Revenues | $608,150,040 |

| Government Business Enterprises (GBE) | $372,116,860 |

| Corporate Income Tax | $241,723,148 |

| Fuel Tax | $183,667,326 |

| Tobacco Tax | $165,184,729 |

| Mining Tax and Royalties | $115,569,000 |

| Payroll Tax | $113,672,686 |

| Vehicle and Driver Licences | $73,500,000 |

| Corporate Capital Tax | $28,251,176 |

| Total | $6,523,686,938 |

{kind=link}

Provincial Revenue Sources: Descriptions

Offshore Oil Royalties: Offshore royalties received by the Provincial Government are governed by clear regulations and royalty regimes, supplemented by specific royalty agreements with the operators of each offshore oil development. For all offshore petroleum projects, benefits agreements are negotiated with project operators and provide the province with royalties, as well as employment commitments and targets, and industrial benefits.

Personal Income Tax: Personal income tax is a tax that is applied to each individual resident of the province and is calculated based on the amount of personal income earned during the taxation year. The current personal income tax rates for Newfoundland and Labrador are as follows:

- 7.7 per cent on the first $35,008 of taxable income + 12.5 per cent on the next $35,007 + 13.3 per cent on the amount over $70,015

Sales Tax: Sales tax is a tax paid for the sales of certain goods and services. Sales tax is typically applied by both the provincial and the federal governments. Within Newfoundland and Labrador, provincial sales tax and the federal sales tax are combined (harmonized sales tax) and currently set at a rate of 13 per cent (8 per cent provincial and 5 per cent federal). Additionally, a retail sales tax of 14 per cent is applied to the private sale of motor vehicles (note that vehicles sold by someone registered with the Canada Revenue Agency as a HST registrant, is not subject to the 14 per cent retail sales tax, as the 13 per cent HST tax rate would apply).

Other Revenues: Other Revenue Sources, such as:

- Insurance Companies Tax

- Investment Earnings

- Other Fees and Fines

- Other Provincial Taxes

- Federally Cost Shared Programs

Government Business Enterprises (GBE): Revenues collected from Nalcor and the Newfoundland Liquor Corporation.

Corporate Income Tax: The Corporate Income Tax is the tax payable by a corporation each taxation year and is equivalent to 14 per cent of the corporation’s taxable income earned in the year in the province. Organizations paying a corporate income tax may be eligible for various tax credits such as:

- Manufacturing and Processing Tax Credit – corporations earning a profit by carrying out manufacturing and processing from a permanent establishment located in province may qualify for a reduced corporate income tax rate of 5 per cent

- Small Business Tax Credit – corporations whose profits categorize them as a small business have a reduced corporate income tax rate of 3 per cent

Fuel Tax: A fuel tax is an excise tax imposed on the sale of fuels primarily intended for transportation. Within Newfoundland and Labrador, the following motive fuel tax rates apply:

| Motive Fuel Type | Tax Rate |

|---|---|

| Gasoline | 16.5 c/L |

| Diesel | 16.5 c/L |

| Auto Propane | 7.0 c/L |

| Marine Fuel | 3.5 c/L |

| Aviation Fuel | 0.7 c/L |

Tobacco Tax: Tobacco tax is a tax that is applied to all tobacco products sold in the province. Tobacco products include cigarettes, cigars and fine-cut tobacco. The following tax rates currently apply within this province:

| Tobacco Product | Tax Rate |

|---|---|

| Cigarettes | 23.5 cents per cigarette |

| Fine-cut Tobacco | 38 cents per gram |

| Cigars | 125 per cent of purchase price |

Mining Tax and Royalties: A Mining Tax of 15 per cent is currently imposed on the net income of mine operators. Additionally, a Mineral Rights Tax of 20 per cent is imposed on the recipient of mineral production royalties, less certain deductions (e.g., legal expenses incurred in the collection of royalties and payment of rents or royalties to other persons).

Payroll Tax: The Health and Post-Secondary Education Tax (more commonly known as the Payroll Tax) is a tax imposed on remuneration that is paid or credited to employees. This tax is paid by employers with an establishment in Newfoundland and Labrador. The present payroll tax rate is 2 per cent of total payroll less the exemption threshold, which is currently $1.2 million.

Vehicle and Driver Licences: Currently the province imposes a passenger vehicle registration fee of $140 annually ($91 for seniors) and a driver licence renewal fee of $100, charged every 5 years ($65 for seniors).

Corporate Capital Tax: In Newfoundland and Labrador, the Corporate Capital Tax is a tax that is applied to any financial institution (banks, loans and trust companies) with permanent establishment in the province during the taxation year. A rate of 4 per cent is payable on capital allocated to Newfoundland and Labrador including paid-up capital stock, contributed surplus, retained earnings, long-term debt, and reserves. For financial institutions with aggregate capital less than $10 million, the first $5 million is exempt from the tax.

- Canada Health Transfer (CHT): Annual transfer from the Federal Government to support long-term predictable funding for health care, in accordance with the principles of the Federal Canada Health Act, which are universality, comprehensiveness, portability, accessibility and public administration.

- Social Transfer (CST): Annual transfer from the Federal Government to support post-secondary education; social assistance and social services; early childhood development; and early learning and childcare.

- Other: This includes annual transfers from the Federal Government such as statutory subsidies and sector-specific subsidies.